|

|

Why the President's Social Security Proposals Could Ultimately Lead to the Unraveling of Social Security

By Jason Furman, Robert Greenstein, and Gene Sperling, The Center on Budget and Policy Priorities

May 2, 2005

Proponents of progressive price indexing present it as a way to protect low-income workers from Social Security benefit cuts and to moderate the effects on middle-income workers, while reducing benefits most for high-income workers. Careful examination suggests, however, that the combination of progressive price indexing and the private accounts that President Bush has proposed would pose serious risks to all workers, because such a package could put Social Security on a path likely to weaken support greatly for Social Security over time.

To be sure, making the Social Security benefit structure somewhat more progressive is desirable, although doing so creates some political risk for the program. But when progressive price indexing is coupled with the President's private accounts, the political risk escalates sharply, because middle-income as well as more affluent workers would eventually get only a tiny Social Security check - or no check at all - despite having paid considerable payroll taxes into the Social Security system.

. Progressive price indexing represents a large benefit cut. While the deepest benefit reductions would fall on those with earnings at or above the Social Security payroll tax cap (now $90,000 a year), workers who earn much less than that would face very substantial benefit reductions as well.

* A medium earner (one who earns $36,600 today) retiring in 2055 would

face a 21 percent reduction in his or her Social Security benefits

(relative to the current benefit structure).

* A worker who earns 60 percent above the average wage - about $59,000

today - and retires in 2055 would face a 31 percent benefit cut.[2]

(These figures are based on the Social Security actuaries' analysis of

the progressive price indexing proposal.)

* For those retiring in subsequent years, the benefit reductions would be

significantly larger.

The benefit cuts would be this large because progressive price indexing is designed to reduce benefits enough to close 70 percent of Social Security's 75-year funding gap by itself. Plans that include progressive price indexing thus rely heavily on benefit reductions to restore Social Security solvency, rather than on a balanced mix of benefit reductions and revenue increases as was done in 1983.

. Under the private accounts that the President has proposed, the cost of the accounts would be offset by reducing the Social Security benefits of those electing the accounts. For every dollar in payroll taxes that a worker diverted from Social Security to an account, the worker's Social Security benefits would be cut a dollar plus an interest charge equal to three percent above inflation. Thus, under the proposal to combine progressive price indexing with private accounts, Social Security benefits would be lowered twice - once due to the indexing changes, and a second time to pay for the private accounts.

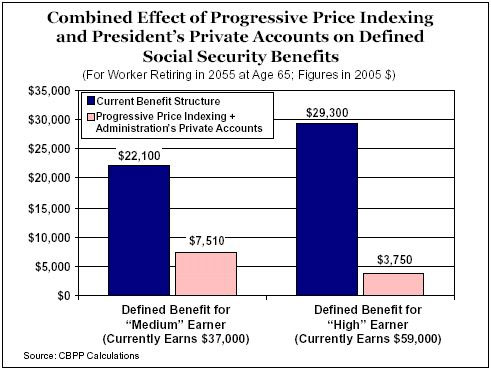

. The result would be that millions of middle-income workers would receive little or no Social Security benefits in retirement. They would largely be left with only their private account.

* For a medium earner who retired in 2055, the defined Social Security benefit would be reduced by 66 percent - from $22,100 a year to $7,510 (in 2005 dollars).

* For a worker who earns 60 percent above the average wage (about $59,000 today), the reduction in Social Security benefits would be 87 percent - from $29,300 a year to $3,750 (in 2005 dollars), or a reduction of more than $25,000 a year. (See graph above and Table 1.)

. As noted, the reductions in Social Security benefits would grow still deeper in subsequent years. For a worker earning 60 percent above the average wage who retired in 2075, the reduction in defined Social Security benefits would be 97 percent. (See Table 2.)

. Furthermore, these figures reflect Social Security benefits before Medicare premiums are subtracted. Medicare premiums are collected by being deducted from Social Security checks. Since Medicare premiums grow at the rate of health care costs, which is faster than either prices or wages, they will consume a steadily increasing share of Social Security benefits over time.

. For many middle-income workers, Medicare premiums would consume most or all of the very small monthly Social Security benefit that would remain under the combination of progressive price indexing and the President's private accounts. Social Security checks for millions of ordinary American workers would be close to or at zero.

If this occurred, the stage would be set for advocacy campaigns to be mounted calling for private accounts to be expanded and to replace much or all of what remained of Social Security. After all, workers would appear to have placed 8.4 percent of their wages in Social Security but to be receiving little or nothing in return. The miniscule Social Security benefits that many workers would receive under the combination of progressive indexing and private accounts would almost surely be seized upon by some on the political right to argue that Social Security had become a terrible deal for American workers and that workers would benefit greatly from converting much or all of what remained of Social Security to private accounts.

Stated another way, the combination of progressive price indexing and carve-out private accounts would likely lead millions of Americans to undervalue Social Security (and to overvalue their private accounts). Their private account might lose money for them; for many workers, the accounts might earn less than the amount that their Social Security benefits would be reduced to offset the cost of the accounts. But people nevertheless could appear to be getting more for the four percent of their wages placed in their accounts than for the 8.4 percent that went to Social Security, especially if they never became disabled and did not need Social Security disability benefits.

Progressive price indexing presents one other serious problem, as well: it is unsound economics. It cuts Social Security benefits (relative to the current benefit structure) by the degree to which wages outpace inflation. As a result, the more that real wages grow, the deeper the reduction in Social Security benefits would be. If the economy performed better in future decades than is currently forecast, the Social Security benefit cuts would be larger even though the stronger economic growth would cause the Social Security shortfall to become smaller. The Congressional Research Service recently took note of this serious design flaw in the proposal in an analysis of progressive price indexing, in which CRS stated: "Thus, somewhat paradoxically, if real wages rise faster than projected, price indexing [either full price-indexing or progressive price-indexing] would result in deeper benefit cuts, even as Social Security's unfunded 75 liability would be shrinking."[3] For each dollar such workers divert to new private accounts, their Social Security benefits would be cut one dollar plus an interest charge equal to three percent above inflation.

The President's Proposal: Progressive Price Indexing and Carve-out Private Accounts

The private accounts that President Bush has proposed would be financed by additional benefit reductions in Social Security for those who elect the private accounts. For each dollar in payroll taxes that workers directed to private accounts, their Social Security benefits would be cut by a dollar plus an interest charge equal to 3 percent above inflation. If progressive price indexing is included in a Social Security plan alongside private accounts of this nature, Social Security benefits thus will be cut twice for workers who elect the accounts, other than people in the bottom 30 percent of the wage distribution (who would not be affected by progressive price indexing).

The combined effect of these two benefit reductions would be dramatic, and not just for high-income workers. Tables 1 and 2 show the level of Social Security benefits under: 1) the current benefit structure; 2) progressive price indexing; and 3) progressive price indexing combined with private accounts structured as President Bush has proposed.

Table 1 shows the effects on workers who are 15 years old today and retire at age 65 in 2055. As the table shows, with progressive price indexing and the President's private accounts, Social Security's defined benefit would drop dramatically for everyone except low earners.

. By 2055, Social Security defined benefits for medium earners - those roughly in the middle of earnings scale - would drop 66 percent, or two thirds, compared to the current benefit structure. (A medium earner in 2005 makes $36,600.) Instead of receiving a Social Security benefit of $1,844 a month in today's dollars (or $22,709 a year), the worker's benefit would be $626. The worker also would have a private account that would be subject to market risk.

. In addition, the group whom the Social Security actuaries label "high earners" -workers whose average earnings are 60 percent above those of the medium earner, or $59,000 today - would face a Social Security defined benefit cut of 87 percent in 2055. Instead of a monthly Social Security benefit of $2,441 in today's dollars, their benefit would be $311.

Table 1

|

Annual Social

Security Benefit For Workers Retiring in 2055

(Benefits in 2005 dollars, does not include the value of private

accounts)

|

|

|

Current-law

Formula

|

With

Progressive Price Indexing

|

With

Progressive Price Indexing and Benefit Offsets for 4% Accounts

|

Percentage

Change

|

|

Low earner (earnings of $16,470 today)

|

$13,413

|

$13,413

|

$8,906

|

-34%

|

|

Medium earner (earnings of $36,600)

|

22,097

|

17,545

|

7,513

|

-66%

|

|

High earner (earnings of $58,560)

|

29,296

|

20,214

|

3,750

|

-87%

|

|

Maximum earner (earnings of $90,000)

|

35,751

|

22,666

|

2,717

|

-92%

|

|

Source: Calculations based on Social Security

Administration, Office of the Chief Actuary, "Estimated

Financial Effects of a Comprehensive Social Security Reform

Proposal Including Progressive Price Indexing -- INFORMATION,"

February 10, 2005 and "Preliminary Estimated Financial Effects

of a Proposal to Phase In Personal Accounts - INFORMATION,"

February 3, 2005. Note that the 4% accounts are assumed to have a

maximum contribution of $1,000 in 2009, growing by $100 per year

plus wage inflation, along the lines proposed by the President.

|

After Medicare Premiums Are Subtracted, Many Retirees Would Receive No Social Security Benefit at All

Moreover, many of these individuals would receive no Social Security check at all. Medicare premiums are collected by being subtracted from Social Security benefits; the Social Security checks sent out each month equal a beneficiary's Social Security benefit minus his or her Medicare premiums. Medicare premiums rise at the same rate as health care costs, which is to say, considerably faster than wages or the general inflation rate. As a result, with each passing year, Medicare premiums consume a larger proportion of Social Security benefits.

. The figures just cited - that by 2055, the combination of progressive price indexing and the Administration's private accounts would eliminate 66 percent of the Social Security benefit for median earners, and 87 percent for so-called "high" earners - reflect the Social Security benefits that would remain before Medicare premiums are taken into account.

. It is from these greatly reduced benefit amounts that the premiums for Medicare physicians' coverage (Medicare Part B) and the prescription drug benefit (Medicare Part D) would be subtracted. The Social Security check that beneficiaries received would be what was left. For millions of workers, the amount of the monthly Social Security check would be at or near zero.

The crunch would become even more severe after 2055. By 2075, as Table 2 shows, the combined effect of progressive price indexing and the President's private accounts would be to reduce Social Security defined benefits by 73 percent for medium earners and 97 percent for the so-called "high earners," even before Medicare premiums are taken into account.

Table 2

|

Table

2

|

|

Annual Social

Security Benefit For Workers Retiring in 2075

(Benefits in 2005 dollars, does not include the value of

private accounts)

|

|

|

Current-law

Formula

|

With

Progressive Price Indexing

|

With

Progressive Price Indexing and Benefit Offsets for 4% Accounts

|

Percentage

Change

|

|

Low earner (earnings of $16,470 today)

|

$16,599

|

$16,599

|

$11,022

|

-34%

|

|

Medium earner (earnings of $36,600)

|

27,344

|

19,715

|

7,301

|

-73%

|

|

High earner (earnings of $58,560)

|

36,254

|

21,100

|

1,233

|

-97%

|

|

Maximum earner (earnings of $90,000)

|

44,236

|

22,428

|

0

|

-100%

|

|

Source: Same as Table 1

|

In other words, this approach ultimately would decimate traditional Social Security benefits for most workers. As a result, it would raise serious questions about whether the Social Security system would remain politically viable. With private accounts being financed through reductions in Social Security benefits rather than in the private-account balances, this approach would make it appear as though most workers were contributing 8.4 percent of their wages to Social Security and getting little or nothing back. Workers would appear to be getting much more back for the four percent of wages they placed in their private accounts.

The difference would reflect, in part, the fact that the costs of the private accounts were being recouped through reductions in Social Security benefits rather than in the account balances. The reductions could be made directly in the account balances, but most private-account proponents do not favor that, because the accounts would then appear less attractive. The difference between Social Security pay-outs and pay-outs from private accounts also would reflect the fact that a portion of Social Security payroll taxes go for disability and survivors insurance, for raising the benefits of retirees who have worked at low wages, and, most importantly, to cover the "legacy debt" that Social Security inherited as a result of the decision made when the program started 65 years ago to cover people who were retiring at that time and had paid little or nothing into the system because Social Security wasn't yet in existence during most of their work careers. (See the box on below for a further discussion of these issues.)

It is unlikely that a system under which Social Security appeared to be such an abysmal deal when compared to private accounts would be politically sustainable over time.

|

Are Private

Account Plans Designed to Devalue Social Security?*

Social Security is a compact among

all Americans designed to ensure a modicum of economic dignity no

matter what life may bring. Much of the value of Social

Security lies in its role as insurance against the threat to

economic dignity that can come through disability, the early death

of a provider, poverty, or living to a very old age and exhausting

one's savings. One-third of Social Security benefits now

go to survivors or workers who have become disabled and their

dependents.

Advocates of replacing part of

Social Security with private accounts often paint a distorted

picture of Social Security's value by describing it only in

terms of its "return on investment." No one would think

it made sense to tell parents who had purchased auto and fire

insurance that they had been terrible investors and had robbed

their children of their inheritance because, with no accidents or

fires, they had a negative return on their insurance premiums.

That would be a distorted frame for assessing the value of

insurance; you hope you never need it, but insurance can make all

the difference for a family if life takes a difficult and

unexpected turn.

Many private-accounts plans are

designed in such a way that Social Security recipients would be

likely to undervalue the benefits of Social Security and to

overvalue their private account. Most "carve-out"

private-account plans, such as the plan the President has

outlined, are designed in a way that is likely to lead people to

think the accounts are a better deal than they are, because the

plans obscure the fact that the accounts have a large cost that

must be incurred. The White House purposely designed its

proposal so that the "offset" (i.e., the reduction in benefits

needed to pay for the accounts) would not be taken out of the

accounts themselves, but out of Social Security checks instead.

A more transparent design, under which the Social Security Trust

Fund would be paid back directly from the account balances, rather

than by cutting Social Security benefits, would make the accounts

look much more modest to beneficiaries and traditional Social

Security benefits look more robust.

Moreover, most private-account

proposals would make Social Security appear to be a worse deal

relative to private accounts than would be the case, for another

reason as well. A substantial share of the payroll taxes

dedicated to Social Security are used to finance the cost of

survivors and disability benefits and of raising benefits for

those who worked for low wages throughout their careers. Any

structure that encourages beneficiaries to compare the monthly

check they receive from private accounts to the monthly retirement

check that Social Security provides thus is likely to lead to

serious misunderstanding by workers and beneficiaries of the

relative value of the two systems.

The architecture of plans designed

to integrate private accounts into the Social Security system,

whether by intent or effect, consequently would create a distorted

picture of Social Security that ultimately could lead many people

to favor measures allowing them to withdraw from Social Security

to a greater degree. These plans thus run the risk of

starting the nation down a slippery slope toward a greater

weakening of Social Security and its vital social insurance

functions.

Social Security has been the crown

jewel of U.S. social programs for decades, in no small part

because it is a compact not only across the generations but also

among all working Americans - the healthy and the middle class

as well as those who work for low wages and those who suffer from

disabilities. Unraveling this compact would make ours a very

different, and less humane, society.

__________________

*

This box is drawn from an April 1, 2005 Memorandum ("Open Letter

to Progressive Policymakers") written by Gene Sperling and

issued by the Center for American Progress.

|

End Notes:

[1] Gene Sperling is a Senior Fellow at the Center for American Progress. Jason Furman is a non-resident Senior Fellow, and Robert Greenstein is Executive Director, of the Center on Budget and Policy Priorities.

[2] For further analyses of progressive price indexing, see Jason Furman, "An Analysis of Using "Progressive Price Indexing" to Set Social Security Benefits," Center on Budget and Policy Priorities, March 21, 2005.

[3] "Progressive Price Indexing" of Social Security Benefits, Congressional Research Service, April 22, 2005.

|

|