|

||||||

|

|

Some related articles : |

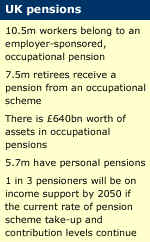

Pensions for

beginners

BBC

News, April 2, 2001

The Financial Services Authority regulates many kinds of

financial business, including pensions Pensions are really terribly

important, especially at a time when the government is talking of reducing

dependancy on the State Pension. The problem is that for many people

choosing a private pension can be terribly confusing. Working Lunch

unravels the maze. Even after you've chosen your pension you still have to choose an annuity and making the right choice can means thousands of pounds more in your pocket. Annuities Although we say 'living off your

pension', what we actually mean is we live off our annuity. If

you have a private pension you contribute to your pension pot for years

and then when you get to retirement age, you take the pot and buy an

annuity. Your annuity pays you a regular amount of money each month until

you die. The

problem is that the amount you get for the whole of your retirement is

dependent on the interest rate at the date of retirement. And that's not

been very good. Annuity rates have fallen recently from nearly 9% to about

5%.

With

the value of the state pension falling, private or occupational pensions

are increasingly important Shopping

around That's

the bad news, so what can you do about it. Well you can shop around for

best annuity rates. Just because you have your pension with one company,

doesn't mean you have to buy the annuity from them. And

here is an example of just how much you can make, by taking some time over

the decision. The difference between one of the best and one of the worst

annuities at the moment (quoted by the Annuity Bureau) would mean this for

your bank balance: £1,030

a year for a man aged 60 (a 21% difference) £1,322

a year for a woman aged 60 (a 31% difference) The

Annuity Bureau and Annuity Direct provide independent advice on annuities.

Income

draw-down Since

1995 you can opt for income draw-down which allows you to take money

directly from your pension pot instead of buying an annuity. Income

draw-down contracts (also known as a Flexible Pension or Pension Fund

Withdrawal) are offered by most pension companies for those with a fund of

at least £100,000. This

allows you to defer the purchase of an annuity until age 75, while still

drawing a limited, but regular, income. Staggered

Retirement

An

alternative approach is known as Staggered Retirement or Phased

Retirement. Many people who purchase a pension annuity do not take out any

form of built-in protection against inflation. Again you have to be

finished with it by the time you are 75 years old. But it enables you to

take part of your pension now and leave the rest until later. There

are lots of restrictions which limit the amount you can take and there is

a danger that you will destroy your capital. It is worth considering, but

once you are 75 you have to go for a proper Annuity. The

Income Drawdown Advisory Bureau is an independent specialist which will

advise on income drawdown, as well as phased retirement and annuities. With-Profit

Annuities Finally

there are a few companies which offer "With-Profit Annuities".

This enables you to buy an annuity with a guaranteed minimum monthly

payout but then you get extra money if the fund in which the money is

invested performs well. There

are only three major companies offering these policies at the moment and

you do want to take careful advice before buying any annuity. There is

some risks attached because if the fund does not perform well then you

won't earn as much money. But

because even With-Profit funds have a guaranteed minimum, the risks are

limited. And this may be a way to help you combat the challenge of living

off low interest rates. Several

important changes have affected the pensions industry over the last few

years. Here we provide a summary of the ongoing overhaul in legislation

relating to pensions:

Personal

pension mis-selling

In

1994 the SIB (now the Financial Services Authority) acted to clean up the

pensions industry following claims that many people sold private pensions

would have been better off remaining in or joining an occupational scheme.

So the pensions industry was required to review all personal pensions sold

between 29/4/88 and 30/6/94. The

first phase of the review concentrated on "priority" cases -

those who are at or near retirement and those who have died. The deadline

for most firms completing the priority cases was December 1998. The second

phase, for those who are more than 15 years away from retirement, has been

through the consultation process and those who may be affected should have

been contacted in the first three months of 1999. In

May 1997 Treasury Minister Helen Liddell started "naming and

shaming" pension firms who were not tackling the review seriously

enough. Large fines have been levied on the most serious offenders -

though the Pru escaped being fined because it is regulated by the SIB and

not the PIA. Bankrupts

to forfeit personal pensions Bankrupts

face the prospect of having their personal pensions forfeited following a

High Court ruling in Dec 1996. The Landau case ruled that all payments

from bankrupts' personal pensions were assets to be used to pay creditors.

Bankrupts

will now forfeit their entire pension for life. Insolvency practioners are

reviewing bankrupticies going back 10 years. The

Pensions Act 1995

Since

6th April 1997 the Occupational Pensions Regulatory Authority (Opra) is

responsible for ensuring that those who run occupational pensions schemes

meet their legal obligations under the Pensions Act. There

is an Independent Complaints Adjudicator who can suspend or disqualify

trustees. Scheme auditors and actuaries will have to act as

whistle-blowers and tell Opra if they think something is wrong. The

Pensions Ombudsman's role has been extended so he can look into disputes

between trustees and employers. The

Pensions Act states that if money has been removed dishonestly from a

pension scheme the employer must make sure enough money is put back into

the scheme to pay future benefits. If

the employer is insolvent and unable to restore the funds the pension

scheme will be able to claim compensation (up to 90% compensation). This

is administered by the Pensions Compensation Board which will apply a levy

on occupational schemes as required. Trustees

Under

the Pensions Act scheme members have the right to choose at least one

third of the trustees - Member Nominated Trustees (MNT). Employers can opt

out but only if the members, having been given a formal opportunity to

object, are in agreement. A

new minimum funding requirement aims to ensure there's enough money in

final salary schemes to pay pensions if a company goes bust. Fund

must be valued every three years and, if the expert valuers say there

isn't enough money, employers have to increase their contributions to the

scheme. Where

a pension scheme invests in the employer's company Trustees now have to

make sure that no more than 5% of the pension fund's assets are invested

in the employer's shares. Pensions

for divorcees

From

1 July 1996, as part of the Pensions Act 1995, in divorce cases a judge is

obliged to look at pensions. The judge will not be able split a pension,

but will earmark parts of a pension, parts of the death-in-service benefit

and parts of a lump sum payout for the ex-spouse. A

clause on pension splitting has been written into the Family Law Bill,

expected to progress though parliament in the next year. FAIR USE NOTICE: This page contains copyrighted material the use of which has not been specifically authorized by the copyright owner. Global Action on Aging distributes this material without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. We believe this constitutes a fair use of any such copyrighted material as provided for in 17 U.S.C § 107. If you wish to use copyrighted material from this site for purposes of your own that go beyond fair use, you must obtain permission from the copyright owner.

|

||