|

|

Social Security plays key part in retirement

By Gannett News Service

November 30, 2005

Financial experts don't agree on the best age to start taking Social Security - so don't feel bad if you're confused, too.

It's a big decision: Once you make it, you can't revise it.

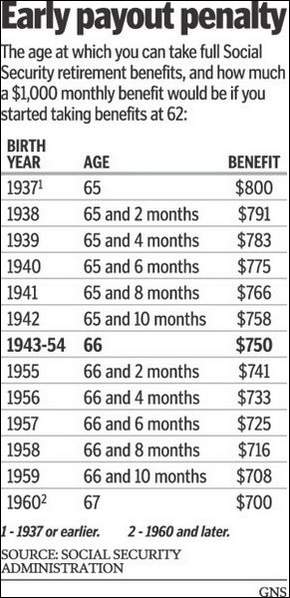

Start by looking at how your retirement age affects your Social Security payout. You can begin to take reduced Social Security benefits at age 62.

The age at which you can get full Social Security benefits depends on when you were born. Those born in 1960 or later can't collect full benefits until they reach 67.

For those born earlier, full benefits kick in between 65 and 67, depending on the year you were born.

You can get an even higher payout by delaying your retirement past your full benefits age. The government increases your payout every month you delay retirement, up to age 70.

Is it better to take lower benefits immediately or wait until you can get full benefits? It depends, in part, on how long you live.

Suppose you're eligible for full benefits at 67, and reduced benefits at 62. If you retire at 62, you get $700 a month, or $8,400 a year. Full benefits at 70: $1,000 a month, or $12,000 a year.

If you take the reduced payment at 62, you'll collect $8,400 a year for five years. That would give you a big head start over someone who starts taking payments at 67.

In fact, the person who starts at 67 would have to live to 78 before earning more in benefits than the person who starts at 62.

You have two other factors to consider before you lock into your Social Security payments:

. Work. If you start taking benefits at age 62 and continue to work, your benefits will be reduced by $1 for every $2 you earn above $12,000 a year. That reduction ends when you reach your full retirement age.

So if your job pays $30,000 a year, your Social Security benefits would be reduced by $9,000.

For the person earning the average benefit of $959 a month, or $11,508 a year, the reduction might not make taking early Social Security worthwhile.

. Taxes. At least part of your Social Security payout may be subject to taxes.

If you're filing jointly and your combined income is $32,000 to $44,000, you'll owe federal income taxes on half your Social Security payment.

If your combined income is more than $44,000, you could owe taxes on as much as 85 percent of your payout.

Financial planners often tell people to start taking Social Security payments as soon as possible. That's an excellent strategy if you plan to retire early. Otherwise, you'd have to draw down your savings until you reach full retirement age.

If you enjoy your job, however, and you don't mind working later in your life, then waiting for the full benefit isn't such a bad idea, particularly given the increase in longevity, says Christine Fahlund, senior financial planner at T. Rowe Price. You'll get the higher payout, adjusted for inflation, as long as you live.

And if you can afford it, waiting until 70 has one benefit: Your payout will increase 8 percent a year. "Not many things in life rise 8 percent a year with a guarantee," she says.

|

|